C3.ai: What You Need To Know About Kerrisdale's Short Allegations

C3.ai: What You Need To Know About Kerrisdale's Short Allegations

The latest frenzy over generative AI – or anything AI-related – has been a boon for software service provider C3.ai (AI). The company saw its share value double in the first quarter, with the run-up picking up pace in March after reporting its eighth consecutive quarter of above-guidance revenues, alongside the announcement of its generative AI product launched earlier this year. But for those who bought the stock at its IPO in 2020 in the $40-range, the position remains 30%+ away from breakeven based on March 31’s closing price.

And the latest short-seller allegations made by Kerrisdale Capital have put any hopes for respite further out of reach. Subsequent to the release of a detailed report explaining its short thesis on C3.ai last month, Kerrisdale has followed up earlier this week with a letter to the attention of the software service provider’s internal audit committee, external auditor, Deloitte & Touche LLP, and the SEC that alleges the company’s engagement in fraudulent reporting.

C3.ai’s share value has declined by almost 40% over the short span of two days following the release of Kerrisdale’s accusations, before paring losses at the end of the short trading week. The following analysis will provide a deep understanding of findings alleged by Kerrisdale. While said allegations remain unproven, we believe the recent findings and accusations by Kerrisdale may lead to incremental caution over the sustainability of C3.ai's fundamental performance in the near-term, and drive further volatility to the stock, effectively overshadowing its recent AI momentum.

Allegations of “Serious Accounting and Disclosure Issues”

Following Kerrisdale’s release of a detailed report of its short thesis on C3.ai last month, which highlights concerns to the sustainability of the software service provider’s fundamental performance, the short-seller has followed up with a letter earlier this week – directed to the attention of Deloitte, C3.ai’s internal audit committee, and the SEC – that claims C3.ai has intentionally engaged in fraudulent reporting. Specifically, Kerrisdale cites it has identified “serious accounting and disclosure issues” in C3.ai’s quarterly and annual filings that might have been incentivized by management’s pressure to meet “sell-side analyst estimates” and “conceal significant deterioration” in the underlying business’ fundamentals performance.

The allegations and concerns identified include:

inadequate disclosures and financial reporting pertaining to C3.ai’s engagement with its “related party and very large customer”, Baker Hughes (BKR);

acceleration in unbilled receivables growth;

improper classification of subscription revenue that in essence mirrors “services- or consulting-oriented revenue”;

overstatement of gross profit margins by inappropriately accounting for costs of revenue as research and development expenses; and

rapid turnover in financial reporting executives

C3.ai's shares lost close to 40% of its market value in the two days after the short-seller letter's release. Prior to market close on Thursday (April 6), the last session of the shortened trading week due to the Easter long weekend, C3.ai has issued a response to some of Kerrisdale's short allegations, including that the short-seller's attribution of all related party transactions disclosed per the company's SEC filings to the Baker Hughes arrangement is simply untrue. C3.ai has also provided examples to support adequacy of its reporting over unbilled receivables. Following the release of C3.ai's response, the stock pared its losses for the week at about 33%.

Accusation 1: Inadequate Disclosures and Financial Reporting for Baker Hughes Arrangement

Baker Hughes, the oil and gas services provider, has entered into a strategic partnership with C3.ai in 2019 prior to the latter’s IPO. Baker Hughes is considered both a significant customer to C3.ai, accounting for the bulk of its quarterly and annual revenues, and a shareholder of C3.ai to which it has a right to appoint a director.

“Some of our customers and other business partners are affiliated with certain of our directors or hold shares of our capital stock, or both. For example, in June 2019, we entered into a strategic collaboration agreement with Baker Hughes whereby Baker Hughes had a right to appoint a director. Our director, Lorenzo Simonelli, is an employee of Baker Hughes, and Baker Hughes is a stockholder.”

Source: C3.ai S-1 Filing, November 2020

In 2019, C3.ai had formed a joint alliance with Baker Hughes in the development of BHC3.ai – a brand of Enterprise AI solutions catered to the oil and gas industry. Under the strategic partnership, Baker Hughes is both a direct customer of C3.ai’s subscription and professional services, and a distribution partner of both C3.ai and BHC3.ai services to end customers.

As part of the original arrangement established in June 2019, C3.ai and Baker Hughes had entered into a three-year agreement with the following terms:

Baker Hughes must directly subscribe to the C3 AI Application Platform, with a minimum annual direct subscription fee commitment of $39.5 million per year for three years;

Baker Hughes is granted an exclusive right to resell C3 products worldwide in the oil and gas industry;

Baker Hughes is granted a non-exclusive right to resell C3 products worldwide in other industries; and

Baker Hughes is required to generate a minimum annual revenue commitment that combines the $39.5 million minimum annual direct subscription fee commitment and sales of C3 products to end customers. This essentially makes Baker Hughes both a direct customer of C3 products, as well as a distribution partner of C3 products, allowing revenue generated from both means to be recognized into C3.ai’s books. The minimum, non-cancellable annual revenue commitment is as follows:

In June 2020, C3.ai and Baker Hughes amended the original agreement to include a two-year extension, with the arrangement expiring April 30, 2024, and revised the minimum annual revenue commitment amounts:

In October 2021, the arrangement was further amended to include an additional year term that would extend the expiry to April 30, 2025. Beginning fiscal 2023, Baker Hughes’ minimum annual revenue commitment will be “reduced by any revenue [C3.ai generates] from certain customers”. This likely means Baker Hughes’ minimum annual direct subscription fee commitment of $39.5 million has been eliminated, with the adjusted minimum annual resell commitment effectively reduced by whatever C3.ai sells during the year to an undisclosed list of pre-determined end customers beginning fiscal 2023. The revised minimum annual revenue commitment amounts from Baker Hughes under the October 2021 amendment are as follows:

Under Baker Hughes and C3.ai’s arrangement, the latter must reimburse the former sales commission for any sales to end customers in excess of the minimum annual revenue commitment. Essentially, C3.ai recognizes subscription and services revenue generated from sales brokered by Baker Hughes to end customers, while Baker Hughes recognizes commission revenue from its distribution of C3 products to end customers.

In January 2023, the arrangement was amended again to accelerate Baker Hughes’ payment terms (i.e. speed up collection). Baker Hughes also obtained expanded reseller rights under the January 2023 amendment, and C3.ai has committed to providing Baker Hughes with incremental products and services. The “potential variable consideration” – which refers to amounts previously attributable to sales C3.ai makes to the undisclosed list of pre-determined customers that would reduce Baker Hughes’ minimum annual revenue commitment – is eliminated under the January 2023 amendment. Coupled with expanded reseller rights granted to Baker Hughes and incremental products and services provided by C3.ai to Baker Hughes, the transaction price attributable to the contract is thus expanded. The amendment has not detailed any adjustments to the minimum annual revenue commitment amounts disclosed in the October 2021 amendment, thus it is assumed that these numbers have not been changed.

Per Kerrisdale’s letter to C3.ai’s internal and external auditors, and the SEC, the short-seller has accused C3.ai of inadequate and unclear disclosures pertaining to its relationship with Baker Hughes. Yet, based on our understanding on the continuity of disclosures pertaining to C3.ai and Baker Hughes’ related party transaction relationship, the contractual arrangement that exists between the two – which is inclusive of the relationship of the two parties, performance obligations, timespan and consideration involved – have been clearly presented.

Accusation 2: Acceleration in the Growth of Unbilled Receivables

One of the main concerns pointed out by Kerrisdale is the growth acceleration in C3.ai’s unbilled receivables balance in the past three quarters of fiscal 2023, while revenue growth has been subdued with days sales outstanding (“DSO”) – a collection metric for outstanding receivables – climbing to almost 200 days over the same period, which exceeds both the company’s historical average and observations among its SaaS peers like Progress Software Corporation (PRGS), Clearwater Analytics (CWAN), and Alteryx (AYX). Specifically, C3.ai has disclosed in its FY2022 10K filing that invoices are typically “payable within 30 to 60 days”. This could potentially imply degradation in the quality of C3.ai’s fundamentals, and worse, inadequate recognition of revenues, resulting in an overstatement to disguise an allegedly failing business.

What are unbilled receivables?

The summary of significant accounting policies disclosed in C3.ai’s latest 10Q and 10K filings indicate it follows ASC 606 Revenue From Contracts With Customers under U.S. GAAP for revenue recognition accounting.

Under ASC 606, revenue can only be recognized into the statement of operations if, and only if the following criteria are met:

The contract(s) with a customer can be identified – A contract is enforceable when 1) each party’s rights and obligations can be identified, with a transaction price attributable to goods/services involved in the arrangement; 2) there is commercial substance to the arrangement; and 3) the collection of substantially all consideration stipulated in the arrangement is probable;

Performance obligation(s) can be identified within the contract – This refers to the identification of distinct goods / services that the seller has promised and is obligated to transfer / fulfill to the customer;

A transaction price is identified for the contractual arrangement – This refers to the consideration to which the seller is entitled to in exchange for the obligation(s) performed / delivered to the customer;

The transaction price can be allocated to each performance obligation stipulated in the contract – This refers to the agreed consideration between the buyer and the seller for each standalone performance obligation identified in the contract, which, in aggregate, makes up the contract transaction price; and

Recognize revenue when performance obligation(s) are fulfilled – Revenue pertaining to the contract can be recognized by the seller into the income statement if all of the aforementioned revenue recognition criteria are met, and the rights to the goods stipulated in the contract have been transferred or services stipulated in the contract have been fulfilled, and the consideration from the buyer can be measured reliably. The revenue recognition process can be completed at a certain point in time or over time when the right to the promised good / service is transferred / fulfilled.

Typically, the flow of revenue recognition journal entries under ASC 606 is as follows:

Unbilled receivables, which are sometimes referred to as “contract assets”, occurs when revenue recognition criteria under ASC 606 are met, but the bill has not been invoiced to the customer yet. C3.ai typically “invoices customers for subscription fees in annual increments upon execution of the initial contract or subsequent renewal”, but there are occasionally differences in the timing of revenue recognition and the timing of invoicing customers. The flow of revenue recognition journal entries when an unbilled receivable is involved is as follows:

Unbilled receivables are a typical occurrence in SaaS companies like C3.ai due to various reasons. For instance, a customer may be engaged in a multi-year subscription contract (typically 3 years at C3.ai), but is billed annually. While the service continues seamlessly and renews automatically on the first day of the new contract year, the service provider may experience a delay in billing the customer for the service provided, resulting in the timing difference, and inadvertently, unbilled receivable.

So if unbilled receivables are so frequent among SaaS companies, why is it a potential problem for C3.ai? Here are potential implications specific to the software services provider:

C3.ai’s unbilled revenue balance has grown at an accelerated pace in recent quarters that makes it not typical when punt against peers; much of it is also generated from revenue recognized on the sale of subscription and professional services to related party and large customer Baker Hughes

the rapid rate of acceleration in unbilled receivables also indicate potential management control deficiencies in the financial reporting cycle, which could increase the risk of material misstatement

Let’s take a deeper look into what C3.ai’s accounts receivable balance entails:

In C3.ai’s case, the company generates revenue primarily from the sale of 1) subscriptions, and 2) professional services:

Subscription – Subscription revenues are generated from the sale of “term licenses, stand-ready [Center of Excellence] (“COE”) support services, trials of [its] applications, and software-as-a-service (“SaaS”) offerings”. The combination of said performance obligations are identified as one package and a single promise to the customer under the contractual arrangement, with a transaction price attributable to the services and goods bundle. Related revenues are recognized over time under the “time-elapsed output method” given promised services and goods are deliverable over a “renewable, multi-year, fixed fee contract” arrangement that typically spans “three years in duration”.

-Professional Services – Professional services revenue are generated from the sale of “implementation services, training, and prioritized engineering services” incremental to the subscription bundle. Related revenues are recognized over time when or as the service obligation is fulfilled by C3.ai, which is typically arranged as a “fixed fee engagement with a duration of less than 12 months”.

According to Kerrisdale’s findings, and consistent with C3.ai’s latest 10Q disclosures, accounts receivables, inclusive of unbilled receivables, have risen at an accelerated rate in the fiscal third quarter, while recognized revenues over the same period had declined year-on-year.

This is consistent with the acceleration in DSO. Recall from the earlier section where we mentioned C3.ai has disclosed its typical collection period as 30 days to 60 days from the invoice date – but if revenue recognized and services performed are not billed, then no wonder DSO is surging. The rising DSO also indicates that the collection cycle on billed invoices might be extending beyond the typical 60 days after all, which is in contrary to management’s optimism over easing macro-driven headwinds on the company’s sales cycles during the fiscal third quarter earnings call:

You might recall that two quarters ago, I spoke of economic headwinds, lengthening sales cycles, as our customers and prospects anticipated recession. In July and August of 2022, we saw a significant negative change in the business environment with the lengthening of decision cycles, and I caution that the market downturn could be significant…Now as we enter into our fourth quarter, we are seeing tailwinds on from improved business optimism and increased interest in applying C3 AI solutions to address an increasing range of applications across a broadening set of industries…There is a genuine optimism in the marketplace for our solutions. And the overall business sentiment appears to be substantially improving.

Source: C3.ai Fiscal 3Q23 Earnings Call Transcript

More surprisingly, the bulk of C3.ai’s ballooning accounts receivable balance is generated from direct subscription and professional services sales to related party and large customer Baker Hughes. As of the fiscal third quarter end, unbilled receivable from Baker Hughes totalled $79.6 million, or 91% of total unbilled receivables for the period, up from $16.5 million in the same period in fiscal 2022, or 83% of total unbilled receivables for the comparable prior year period. Unbilled receivable from Baker Hughes for the quarter ended January 31, 2023 also represented 30% of C3.ai’s total consolidated revenue generated over the preceding four quarters:

Based on Kerrisdale’s allegations, the observation might imply potential implementation of aggressive accounting measures to inappropriately frontload recognition of revenues pertaining to C3.ai’s long-term sales contract with Baker Hughes.

In the last four quarters, C3.ai has apparently recognized $80 million of receivables (from a related party shareholder, no less) in an amount that is equivalent to almost 30% of total company-wide revenue during that same period, for which it has not even invoiced. It appears to us that C3.ai is booking fictional revenue in order to meet consensus analyst estimates and cover up the fact that, in reality, its products are unable to get traction with customers and its business is failing.

Source: Kerrisdale Capital

For instance, based on the remaining performance obligation (“RPO”) stipulated in C3.ai’s long-term contractual arrangement with Baker Hughes, C3.ai might have frontloaded recognition of revenue pertaining to said performance obligations that might not yet been performed. Without billing Baker Hughes, C3.ai can effectively overstate its top-line by recognizing RPO into revenue without making the customer aware, thus presenting an opportunity for the company to conceal potentially deteriorating financial performance in the consolidated underlying business. Fraud risk is considered significant by default for revenue recognition based on GAAP-based accounting. Specifically, the three components of the fraud triangle – incentive, opportunity, and rationale – are prominent in the process of revenue recognition, which together makes the perfect concoction for fraud. Paired with our mention in the earlier section of how ballooning unbilled revenues could be indicative of poor / deficient management controls on revenue recognition accounting, the opportunity for committing fraudulent reporting accordingly increases.

Up until this point, it does seem like Kerrisdale’s allegations are shaping up nicely. But there could also be alternative narratives to explain for the shocking uptrend observed in C3.ai’s accounts receivable and unbilled receivable balance. While management has not provided any direct feedback on this matter, it remains possible that perhaps there might just have been a higher volume of subscription and professional services provided to C3.ai’s related party Baker Hughes in recent periods, yet invoices just have not been billed nor collected. This is consistent with the increasing balance of sales commission C3.ai has paid to Baker Hughes in recent periods for sales that the latter has made beyond its minimum annual revenue commitment. As of the nine months ended January 31, 2023, Baker Hughes has already delivered $86.8 million in revenue to C3.ai as part of both companies’ joint arrangement, which exceeds the minimum annual revenue commitment of $85 million for fiscal 2023.

The Company and Baker Hughes further revised these agreements in October 2021 to extend the term by an additional year for a total of six years, with an expiration date in the fiscal year ending April 30, 2025, to modify the amount of Baker Hughes’ annual commitments to $85.0 million in fiscal year 2023…

Source: C3.ai Fiscal Year 2022 10K Filing

The Company also agreed to pay Baker Hughes a sales commission on subscriptions and services offerings it sold in excess of [the] minimum revenue commitments…The Company acknowledged that Baker Hughes had met its minimum annual revenue commitment for the fiscal year 2022 and recognized $16.0 million of sales commission as deferred costs during the fiscal quarter ended October 31, 2021 related to this arrangement, which will be amortized over an expected period of five years.

Source: C3.ai F3Q23 10Q Filing

Meanwhile, for fraudulent revenue reporting to have occurred, C3.ai would have had to prove to both its internal and external auditors that a contract with Baker Hughes exists and the performance obligations for the revenue recognized during the period have been met – even if it did not. And this would have been difficult, as auditors typically go through rigorous and extensive substantive and management control testing processes pertaining to the revenue balance given its significant fraud risk nature. Incremental procedure would have been performed by the external auditor to assess incremental risk stemming from the nature of C3.ai’s related party transactions with Baker Hughes.

However, we remain cautious on trends pertaining to revenue, accounts receivables, and unbilled receivables recognized by C3.ai from related party Baker Hughes, given their unusual acceleration relative to peers, and sheer size of the balances’ concentration of the company’s consolidated results. This is further corroborated by the repeated amendments to the minimum annual revenue commitments outlined in their joint arrangement since initiation in 2019 through 2021, which has resulted in declining adjustments indicative of decreased recurring subscription demand both directly from Baker Hughes and indirectly from end customers to which Baker Hughes sells C3.ai’s services to.

Accusation 3: Improper Classification of Subscription Revenue to Overstate Gross Profit Margins

Per its letter, Kerrisdale has also called out improper classification of subscription revenue at C3.ai, which could be misleading investors into thinking the company engages in a high-margin business. The short-seller has also accused C3.ai of improper classification of cost of subscription and cost of professional services revenues into R&D to artificially inflate gross profit margins to better present the company as a high-margin SaaS business deserving of higher valuation multiples. Kerrisdale has also accused C3.ai of potentially inadequately bucketing costs of generating sales into R&D to overstate gross profit margins required to maintain typically higher valuations rewarded to more profitable SaaS business models.

Understanding Revenue Disclosures

Before addressing Kerrisdale’s accusation that C3.ai has improperly classified subscription revenues, the following will provide a brief understanding of revenue disclosures required under U.S. GAAP.

Under U.S. GAAP, revenue can be recognized once the related criteria discussed in the foregoing analysis are met. There is no requirement to “prescribe specific categories for disaggregation” of revenue unless it is needed to meet overall disclosure objectives to comply with ASC 606-10-50-1:

ASC 606-10-50-1 An entity shall disclose qualitative and quantitative information about all of the following:

a. Its contracts with customers…

b. The significant judgments, and changes in those judgments, made in applying [the revenue standard] to those contracts…

c. Any asset recognized from the costs to obtain or fulfil a contract with a customer

Source: U.S. GAAP

And whether disaggregated disclosure of revenue composition is needed is left to the discretion of management. Management must exercise professional judgment to determine if said disaggregated disclosures are required to reasonably comply with ASC 606-10-50-1 revenue disclosures discussed above.

ASC 606-10-55-90 When selecting the type of category (or categories) to use to disaggregate revenue, an entity should consider how information about the entity’s revenue has been represented for other purposes, including all of the following:

a. Disclosures presented outside the financial statements (for example, in earnings releases, annual reports, or investor presentations)

b. Information regularly reviewed by the chief operating decision maker for evaluating the financial performance of operating segments

c. Other information that is similar to the types of information identified in (a) and (b) and that is used by the entity or users of the entity’s financial statements to evaluate the entity’s financial performance or make resource allocation decisions.

ASC 606-10-55-91 Examples of categories that might be appropriate include, but are not limited to, all of the following:

a. Type of good or service (for example, major product lines)…

Source: U.S. GAAP

In C3.ai’s case, the company has appropriately disaggregated its consolidated revenue into two segments relevant to the type of goods / services it provides – subscription and professional services – in order to ensure sufficient qualitative and quantitative information pertaining to how sales are generated are appropriately disclosed in compliance with ASC 606-10-50-1. Yet, Kerrisdale claims inappropriate classification of C3.ai’s subscription revenues on the grounds that significant bespoke work is required to get customers hooked onto C3 subscription products. Specifically, interviews conducted by Kerrisdale with some of C3.ai’s customers suggest that work performed by C3.ai requires substantial tailoring to customer-specific needs. But based on the discussion above on revenue disclosures and revenue recognition, C3.ai does offer C3 AI Application Platform offering subscriptions to customers alongside bundled professional support, to which details of said arrangements have also been appropriately disclosed.

In fact, we are less concerned about C3.ai’s presentation of its subscription revenue, given the company does provide annual subscriptions to its C3 AI Application Platform offerings, bundled with relevant professional services like configuration and training similar to its peers. It appears that subscription revenue and cost of subscription revenue are related to a bundle of C3 subscription products and related professional support, whereas professional services revenue and cost of professional services revenue are related to the provision of incremental consulting and bespoke services outside of C3 subscription products. Under the assumption that total revenue – regardless of how they are disaggregated – is reflective of performance obligations fulfilled by C3.ai during the reporting period, and all related costs of executing said performance obligations have been appropriately reported as total costs of revenue without material misstatement, then disclosure and recognition requirements under U.S. GAAP have been sufficiently met. How it is interpreted is often at the discretion of the user of the financial statements.

Instead, we are more concerned with how C3.ai’s more than 60% gross profit margins reported for its subscription business segment might align with findings from Kerrisdale’s interviews with certain customers of the C3 AI Application Platform. As mentioned in the earlier section, interviews conducted by Kerrisdale with some of C3.ai’s subscription customers indicate lengthen integration processes that typically appear more like a bespoke / tailored professional service. This implies high implementation costs, thus lower subscription margins. However, it is also possible that Kerrisdale’s findings may be skewed and not reflective of less labour-intensive adoption of C3 subscription products at other end customers. This can be corroborated by high-rating customer reviews on C3.ai products found online, which have been spread across years and various industries to support reliability. Recall that SaaS revenues are typically high-margin due to its scalable nature. As long as C3 subscription products are high priced enough, can be efficiently installed and can generate sufficient adoption volume, it is possible to achieve substantial gross profit margin expansion via rapid economies of scale.

C3.ai’s professional services gross profit margins also come at a whopping 90%, which raises concerns given they are significantly higher than those observed across its SaaS peers, and do not really reflect the high labour costs of executing bespoke training and consulting services – unless C3.ai charges an insanely high premium on said services, which is not usually the case observed at its SaaS peers who typically consider professional services as adjacent offerings to their main subscription businesses. But based management commentary from C3.ai’s latest earnings call, it does appear the high margin nature of its professional services business segment may have benefited from premium charges:

…we have various types of professional services, and we have highly skilled workforce, and we’re able to command good premium on those services. And Baker Hughes is one of the customers, many customers whom we – which provide professional services.

Source: C3.ai F3Q23 Earnings Call Transcript

Taken together, C3.ai reports gross profit margin of 67% on its consolidated business. While the figure is consistent with the high margin nature of SaaS operations, signs of fundamental deterioration at the underlying business as analyzed in the earlier section brings about incremental caution. This leads to the next related allegation brought forth by Kerrisdale, which is the fact that C3.ai may be inappropriately allocating costs of revenue to R&D instead to artificially inflate gross profit margins towards levels consistent with the broader SaaS peer group.

Allegation 4: Inappropriate Classification of Cost of Revenue into R&D

Specifically, cost of subscription revenue is defined per C3.ai’s FY 2022 10K filing as spending “related to compensation, including salaries, bonuses, benefits, stock-based compensation and other related expenses for the production environment, support and COE staff, hosting of C3 AI Software, including payments to outside cloud service providers, and allocated overhead and depreciation for facilities”. Meanwhile, cost of professional services revenue primarily consists of “compensation, including salaries, bonuses, benefits, stock-based compensation and other related costs associated with professional service personnel, third-party system integration partners, and allocated overhead and depreciation for facilities”. Essentially, cost of revenue are primarily personnel costs directly relevant to the execution of subscription and professional services sales. On the other hand, R&D expenses are strictly spent on continued development and refinement of C3 AI Software, including the addition of “new features and modules, increasing functionality and speed, and enhancing the usability of C3 AI Software”.

Kerrisdale alleges that C3.ai has inappropriately understated costs of revenue by allocating spending pertaining to human capital required to implement C3 product subscriptions and professional services to R&D instead. Specifically, C3.ai’s R&D spend as a percentage of consolidated revenue has rapidly grown from the 30% range in 2021 to the 80% range in recent quarters. But cost of revenue has also increased over the same period, with gross profit margin declining from the mid-70% range to the 60% range in recent quarters, primarily due to incremental headcount costs, consistent with the hiring spree prior to the latest economic downturn in the broader tech sector.

Higher R&D spending as a percentage of revenue over the past year is also consistent with increased hiring over the same period to support continued build out of C3 products – in line with additional offerings provided to Baker Hughes as observed per the January 2023 amendment to their joint arrangement – as well as the ramp up of funding towards supporting the C3.ai Digital Transformation Institute established in February 2020 alongside Microsoft (MSFT) and leading universities. Related spending will likely remain elevated over the next several quarters as C3.ai engages in the development and deployment of incremental generative AI solutions as announced earlier in the year. As such, Kerrisdale’s allegations that C3.ai may be inappropriately overstating gross profit margins via improper classification of costs in order to reinforce prospects for a higher valuation lacks ground.

Another concern pointed out by Kerrisdale pertaining to C3.ai’s gross profit margins is the nominal costs of generating related party sales to Baker Hughes. Based on C3.ai’s latest fiscal third quarter 10Q filing, the company has generated $20.3 million in related party subscription revenue and $8.6 million in related party professional services revenue in the three months ended January 31, 2023. Yet, related costs of revenue were nil over the same period, potentially implying related party gross profit margin of 100%. However, C3.ai has not disclosed in any filings the extensive list of related party customers, hence it cannot be concluded whether the entirety of related party transaction amounts can be attributed to Baker Hughes. This is consistent with C3.ai’s recent response to Kerrisdale’s statement that the company’s “gross margin from [the Baker Hughes] account is 99% is simply not true and cannot be inferred from [its] financial statements, as [it] does not provide that information on a customer-specific basis”.

When asked about the high profitability of related party sales – especially pertaining to the provision of professional services – during C3.ai’s latest earnings call, management has also pointed to the high gross margin of various “consulting base or more ad hoc” projects in recent quarters compared to “historical implementation services”:

Mike Cikos

Got it. Got it. And one other thing, if I could, but I know you guys obviously cited the better profitability here versus expectations. And one of the -- I guess there were two primary big drivers. The first is we had a large sequential uptick in the pro services revenue and that pro services gross margin. Can you help us think about what drove that strong return in pro services as well as the gross margin there coming in, it was in the 90% plus range, which I think was much higher than what you guys have typically done. Was there any onetime item that benefited that gross margin?

Juho Parkkinen

So we have a highly skilled professional services organization, and we do various projects where we are able to command a high margin. Our standard kind of historical implementation services would be at a lower margin, but then we also do certain consulting base or more ad hoc projects that carry a very high gross margin.

Source: C3.ai F3Q23 Earnings Call Transcript

On this basis, the fluctuations in C3.ai’s cost of revenue and operating expenses in recent quarters seem reasonable considering the nature of its business. In fact, management may have a higher incentive to overstate professional services revenue – which has, in recent quarters, garnered greater margin expansion – than subscription revenue, which potentially contradicts allegations by Kerrisdale analyzed in the earlier section.

Implications for C3.ai

To put the cherry on top of its short-thesis for C3.ai, Kerrisdale has also pointed to the high turnover of financial reporting executives in the company in recent years, with newly appointed CFOs possessing incrementally less experience under their belts. Admittedly, Kerrisdale’s allegations of fraudulent financial reporting at C3.ai – even if not proven – have brought to light some signs of weakening fundamental performance at the company, while also drawing higher professional skepticism among investors on how various financial performance metrics reported by management might not align with actual operating performance at the company. This could very well introduce volatility as a frequent theme for the stock in the near-term, especially as shares rally on the latest AI momentum – even as management suggests they have yet to figure out how to optimize monetization on said opportunities yet:

Gil Luria

My follow-up is it sounds like you're talking about two things. One, about how generative makes your current products we better and another how you can apply it in an enterprise level beyond your product set to other data sets within the enterprise, which one is the bigger commercial opportunity?

Tom Siebel

That's a really good question. And I mean you really asked a good question. And because there is a big opportunity to do this in enterprises that do not use C3 and do not intend to use C3, okay? But they want the unified view of their data. And so the honest answer is we have not figured out how to monetize that yet. We haven't put a price on it yet, but there is potentially a very large market there.

And it's no place -- it's not in any of our operating plans yet, but it will be.

Source: C3.ai F3Q23 Earnings Call Transcript

Beyond Kerrisdale’s latest allegations, we also believe C3.ai has yet to de-risk its forward guidance sufficiently considering the mounting macroeconomic challenges that exist across the demand environment. Specifically, as the company transitions to a consumption-based model, we believe they will become more prone to demand challenges in the near-term as recession risks increase. As discussed in one of our previous coverages, consumption-based business models are typically first to get hit during a recession because of the flexibility offered to customers to scale down usage under the conservative operating environment. Coupled with the broader software and tech industry’s conservative sentiment over the near-term demand environment, with increasing warnings of a “tech recession”, we believe management’s optimistic commentary that business will continue to improve from the challenges previously experienced in mid-2022 may have been premature, and potentially sets up for higher execution risks ahead.

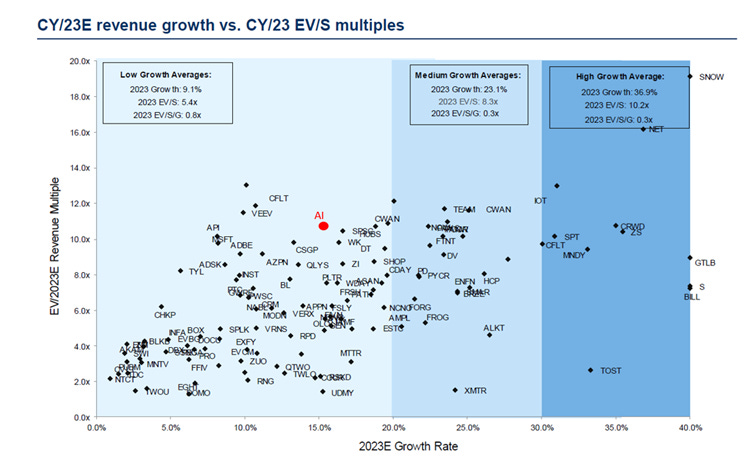

With the C3.ai stock trading at almost 14x estimated ’23 sales and about 12x estimated ’24 sales just a week ago prior to pressure from Kerrisdale’s recent allegations, and still at almost 10x estimated ’23 sales after by the end of the week, it remains expensive relative to peers with similar growth profiles. And with its fundamental guidance likely not yet de-risked enough for looming macroeconomic challenges to the industry’s demand environment, we expect further volatility that would bring into question the sustainability of C3.ai’s relatively overvalued market valuation at current levels.